Closing Costs Explained: 7 Real Estate Closing Secrets to Save Thousands in 2026

The Closing Cost Shock Nobody Warns You About You found the house. You survived the bidding war. You signed the contract. Then your lender sends over a document with a number that makes your stomach drop — closing costs. Suddenly you need thousands of extra dollars you did not plan for, and nobody warned you the bill would be this high. If you have been searching for closing costs explained 2026 — in plain English, with the real estate closing secrets most agents will not tell you — you are in the right place. This guide breaks down exactly what you will owe at the closing table and reveals seven proven strategies to save thousands before you hand over the keys. Here is the short version: closing costs are the fees required to finalize your mortgage and transfer property ownership. They typically run 2% to 6% of the loan amount. On a $300,000 home, that means you are looking at $6,000 to $18,000 in fees before you get the keys. But here is what the industry does not want you to know: almost every one of those fees is negotiable. Everyone sitting at the closing table is making a commission off your deal. The lender, the listing agent, your agent, the title company. They all get paid. And because they all get paid, they can all give a little. This article will show you exactly how to make them do it. What Are Closing Costs? A Quick, No-Fluff Breakdown Closing costs are the bundle of fees required to process your mortgage, verify the property is worth what you are paying, insure the title against old claims, and record the transaction with the county. Think of them as the administrative price of transferring a deed from one person to another, except the price tag is absurdly high and nobody explains it until you are too far in to back out. The standard range is 2% to 6% of the loan amount. On a $300,000 home, that is $6,000 to $18,000. If you are paying cash, do not think you are off the hook. Cash buyers skip mortgage-related fees like origination and underwriting charges, but they still pay for the inspection, the appraisal, and owner’s title insurance. The transaction still has to clear, and someone has to pay for the paperwork. Here is the reality of who pays what: buyers pay a long list of smaller fees. Sellers pay fewer fees, but those fees are enormous. Both sides are funding the same transaction, and both sides have room to negotiate. The sooner you accept that closing costs are a conversation, not a fixed invoice, the more money you will keep. Who Pays What? Buyer vs. Seller Responsibilities Buyers carry the bulk of the line items. You will see origination fees from the lender, which cover processing and underwriting the loan. There is the appraisal fee, the credit report fee, and the lender’s title insurance policy, which protects the bank against ownership disputes. You will prepay property taxes and homeowner’s insurance, often several months at a time, into an escrow account. Recording fees go to the county to make the deed official. Sellers write fewer checks, but the checks are massive. Agent commissions typically run 5% to 6% of the sale price, split between the listing agent and the buyer’s agent. Sellers also pay for the owner’s title insurance policy, transfer taxes, and prorated property taxes up to the closing date. Historically, sellers pay 8% to 10% of the sale price when you include commissions, according to Zillow data. The blunt truth is that buyers feel the sting more. You just drained your savings on the down payment, and now someone wants another six to eighteen thousand dollars. But sellers are writing a check that is often five or six times larger. Both parties have skin in the game, and both parties can negotiate. The next seven secrets will show you how. Real Estate Closing Secret #1: The Seller Concession Power Play A seller concession is exactly what it sounds like. The seller agrees to pay a portion of your closing costs. In practice, this usually means you offer a slightly higher purchase price, and the seller kicks back the difference at closing. You finance the concession into your loan, which spreads the cost over thirty years instead of paying it upfront. Here is the math. On a $300,000 home, a 3% seller concession equals $9,000 toward your closing costs. If you offer $309,000 with a $9,000 concession, the seller nets the same amount, and you bring $9,000 less to the closing table. Your monthly payment increases by roughly forty dollars. For most buyers, that is a trade worth making. Timing matters. Ask for a concession when the seller has leverage to lose. In a buyer’s market, when homes sit for thirty days or more, sellers are far more willing to deal. If the inspection turns up repairs the seller does not want to make, pivot and ask for a closing cost credit instead. The same logic applies if the appraisal comes in low and the seller needs to keep the deal alive. The pro move is to ask for 3% to 6% of the purchase price. FHA loans allow sellers to contribute up to 6%. Conventional loans with less than 10% down cap concessions at 3%, while loans with 10% to 25% down cap at 6%. VA loans allow up to 4%. Know your loan limits and ask for the maximum. The concession is tax-deductible for the seller as a selling expense, and it is cash in your pocket. There is no downside to asking. Real Estate Closing Secret #2: The Broker Concession, the Sassy and Blunt Take Let us talk about the people who stand to make the most money from your deal. The listing agent is collecting 2.5% to 3% of the sale price. Your buyer’s agent is collecting the same. On a $300,000 home, that is $7,500 to

Home Investment Value in 2026: What Makes a Home a Good Investment

A house is a collection of materials you can upgrade, reconfigure, or even tear down. Its location is permanent. That single truth is why location value and neighborhood growth determine whether a home becomes a wealth-building asset or a financial disappointment. Two homes with identical square footage, the same floor plan, and comparable finishes can sell for prices separated by hundreds of thousands of dollars based on nothing more than where they sit on a map. In 2026, as buyers navigate a market shaped by hybrid work patterns, climate awareness, and shifting demographics, knowing how to evaluate location with precision has never mattered more. This article gives you a structured, data-backed framework, the Four Forces of Value, to assess any property with the same lens professional appraisers and lenders use to determine home investment value in 2026 . Table of Contents Why Location Is the #1 Factor in Home Value (The “Unchangeable” Asset) Opendoor research confirms what experienced agents have always known: location is the single most powerful variable in residential real estate pricing. Two identical homes can differ by hundreds of thousands of dollars based solely on their address. The reason is simple. You can replace countertops, refinish hardwood floors, repaint walls, and install a new roof. You cannot change the street your home sits on, the school district it feeds into, or the commute radius it occupies. Location value operates on three distinct levels. The first is the region or metro area, think Atlanta versus a rural Georgia town, where broad economic currents set the baseline. The second is the specific neighborhood, where school quality, crime statistics, and amenity access create micro-markets within the same city. The third is the exact lot and its position on the street, where factors like corner exposure, traffic noise, and orientation to sunlight come into play. Each level compounds the others. In 2026, remote and hybrid work has reshuffled some traditional location preferences, but it has not erased them. Buyers still pay a measurable premium for neighborhoods that offer short commutes to major employment hubs, even if they only make that drive three days a week. What has shifted is the definition of desirable proximity. “Hub-adjacent” suburbs with walkable downtowns, good schools, and access to parks now compete aggressively with urban cores that lost some of their convenience advantage during the pandemic years. The Four Forces of Real Estate Value – A Professional Framework Most articles about home value toss out a random list of factors: schools, crime, parks, jobs. That approach is shallow and hard to apply consistently. The appraisal industry uses a far more disciplined system called the Four Forces of Value: Economic, Social, Governmental, and Environmental. This framework, embedded in Fannie Mae’s Selling Guide for lender appraisals, provides a repeatable method for evaluating location value and neighborhood growth across any market. It also directly answers a question many buyers and investors search for: what actually drives real estate value at the structural level. Economic Forces – Jobs, Income, and Local Market Health A neighborhood’s economic foundation determines whether home values rise, stall, or decline. The most fundamental indicator is employment diversity. A community anchored by a single large employer carries more risk than one with a mix of industries, healthcare, education, technology, manufacturing, logistics, because a layoff event at one company will not crater the entire local housing market. When you evaluate a neighborhood, identify the major employers within a 30-minute drive and ask whether that employment base is growing or contracting. Rising median household income within a ZIP code signals growing purchasing power and increasing demand for housing. When incomes climb faster than home prices, the market has room to run. When prices outpace income growth by a wide margin, the area may be approaching an affordability ceiling that caps future appreciation. Property tax rates and assessment trends add another layer. Two counties in Georgia can have dramatically different millage rates, and those differences compound over years of ownership. A home in a lower-tax jurisdiction effectively returns more net value to the owner, all else being equal. Check recent tax assessment history for the property and its neighbors: a pattern of aggressive reassessments can erode the return you expect. Social Forces – Demographics, Schools, and Community Appeal The social dimension of location value captures how people actually live in and perceive a neighborhood. School district quality sits at the top of this category for good reason. A Realtor.com analysis found that homes in top-rated school districts sell for approximately 49 percent more than comparable homes in average districts. That premium holds even among buyers without school-age children, because resale value depends on the broadest possible pool of future buyers, and families with kids represent a large share of demand. Demographic shifts reshape neighborhoods over time. Millennials, now in their prime family-formation years, are driving demand in suburbs with good schools and walkable amenities. At the same time, aging baby boomers are downsizing, creating demand for single-level homes in communities with low maintenance requirements and proximity to healthcare. A neighborhood that attracts both cohorts has a deeper, more resilient buyer pool. Walkability has moved from a niche preference to a mainstream value driver. Redfin analysis shows that homes with above-average Walk Scores sell for thousands more than similar homes in car-dependent areas. A Walk Score above 70, indicating that most errands can be accomplished on foot, correlates with measurably higher price per square foot. Safety is non-negotiable. Research from the National Bureau of Economic Research confirms that declining crime rates are directly correlated with rising property values. Buyers do not just look at absolute crime statistics; they respond to the trend. A neighborhood where crime is falling year over year signals improving conditions and attracts investment. Governmental Forces – Zoning, Regulations, and Future Planning Government action shapes what can be built, where it can be built, and how much it costs to own property in a given location. Zoning is the most powerful tool local governments wield. Single-family

9 Real Estate Lies People Still Believe in 2026 (And the Truth You Need to Know)

The 2026 housing market looks nothing like it did five years ago. Higher interest rates have cooled the frenzy, but the “lock-in effect” has kept inventory painfully low. Sellers with 3% mortgages are staying put, buyers are stretching their budgets, and somewhere in the middle, a lot of bad information is floating around. People make decisions based on something their neighbor told them, or a number they saw on a website, and it costs them real money. Whether you are buying or selling, separating real estate myths from facts is the only way to win. We are pulling back the curtain on the agent secrets that most people don’t learn until it is too late. Here are nine Real Estate lies people believe in 2026, and what you should believe instead. Table of Contents Myth #1 – Zillow’s Zestimate Is the Same as an Appraisal Zillow has done something remarkable. It has convinced millions of Americans that a computer algorithm can tell them exactly what a house is worth. The Zestimate is an automated valuation model, or AVM. It pulls public records, recent sales data, and tax assessments, then spits out a number. What it cannot do is walk through the front door. It cannot smell the mildew in the basement, see the cracks in the foundation, or notice that the kitchen was renovated with cheap materials that photograph well. The gap between a Zestimate and a real appraisal can be staggering. In some markets, Zillow itself admits its estimates are off by 5% to 10% or more. In rural Georgia counties, where sales are sparse and properties are unique, the error margin can be even wider. The lie here works both ways. Sellers see a high Zestimate and refuse to list for a penny less. Buyers see a low Zestimate and submit an offer that insults the seller. Both sides lose because neither number is real. An appraisal is the only valuation that matters when a mortgage is involved. A licensed appraiser visits the property, compares it to similar homes that actually sold, and adjusts for condition and location. Zillow is a marketing tool. It is a starting point for conversation, not a closing argument. Treat it that way. Myth #2 – You Must Put 20% Down to Buy a Home This is the myth that keeps more renters trapped than any other. The idea that you need a giant pile of cash to buy a house is so deeply embedded in American culture that people stop even checking whether it is true. It is not true. It has not been true for decades, and it is especially not true in 2026. FHA loans allow qualified buyers to put down as little as 3.5%. Conventional loans backed by Fannie Mae and Freddie Mac offer programs with just 3% down. If you are a veteran or buying in a rural area, VA and USDA loans can get you into a home with zero down. These are not fringe products. They are mainstream lending programs used by first-time buyers across Georgia and the rest of the country. The objection people raise is Private Mortgage Insurance, or PMI. Yes, you will pay PMI if you put down less than 20%. But run the math. If you wait five years to save a 20% down payment while home prices rise 3% to 4% annually, you may never catch up. The house you want at $300,000 today could cost $345,000 by the time your savings account is full. Paying PMI for a few years while building equity often beats waiting. In 2026, the real barriers to buying are credit score and debt-to-income ratio, not the size of your down payment. Myth #3 – Offering More Than Asking Price Guarantees You Win In a competitive market, the instinct is to swing big. Throw out a number well above asking price, and the seller will surely pick you. This logic falls apart the moment an appraisal comes back low. Imagine a house listed at $320,000. You offer $350,000 because you want to blow the other offers away. The seller accepts. Then the appraiser walks through and says the house is worth $320,000. The bank will only lend based on that $320,000 appraisal. You now have a $30,000 gap to cover in cash. If you do not have it, the deal collapses. The seller goes back to square one, and you have wasted weeks and an inspection fee. Savvy sellers understand this. They often prefer a clean offer at $325,000 with a strong pre-approval letter and a buyer who promises not to nickel-and-dime them on repairs. A high offer with shaky financing is a gamble. A reasonable offer with solid terms closes. In 2026, terms matter as much as price. Cash, quick close, and appraisal gap coverage are the levers that win deals, not just a big number on the contract. Myth #4 – Asking for a Home Inspection Will Kill the Deal Somewhere along the way, buyers got the idea that asking for repairs after an inspection makes them difficult. That a seller will rip up the contract the moment a request comes through. This fear is what pushed so many buyers during the pandemic frenzy to waive inspections entirely, a decision some of them now regret deeply. An inspection request is not a demand. It is a conversation. A reasonable buyer does not ask the seller to fix a squeaky door or repaint a bedroom. They ask about safety issues, structural problems, and major systems that are failing. A roof that leaks, a furnace that is dead, a electrical panel that is a fire hazard. These are things any rational seller should expect to address, because any other buyer will flag the same issues. In 2026, sellers are more willing to negotiate on repairs than they were a few years ago. The market has shifted. Buyers have more leverage, and a seller who kills a deal over a legitimate inspection finding is cutting off

The 2026 Home Inspection Checklist for First-Time Buyers in Georgia: Termite & Foundation Focus

You found a house. The kitchen has granite counters, the backyard is perfect for a fire pit, and you are already picturing where the couch goes. Then your agent mentions the inspection, and a knot forms in your stomach. That knot is justified. In Georgia, a standard walkthrough is not enough. The soil, the humidity, and the bugs conspire against a home’s bones in ways that a fresh coat of paint hides easily. This home inspection checklist for first-time buyers in Georgia termite and foundation focus is built to cut through the cosmetic shine and zero in on the two things that can bankrupt a new owner: the structural slab under your feet and the silent insects eating the walls. By the time you finish reading, you will know exactly what to look for, what questions to ask, and how to walk into closing with your eyes wide open. Table of Contents Why Georgia First-Time Buyers Must Prioritize Termite and Foundation Inspections in 2026 Georgia sits in a high termite-pressure zone that makes a standard home inspection insufficient without a dedicated Wood Destroying Insect report. These pests are called silent destroyers for a reason. By the time you spot mud tubes crawling up a foundation wall or find a pile of frass on a windowsill, a colony has likely been chewing through floor joists and studs for months or even years. The repair bill for that kind of structural damage often reaches thousands of dollars, and your homeowners insurance policy will almost certainly not cover a dime of it. The ground itself presents a separate threat. Georgia’s expansive clay soil swells when wet and shrinks when dry, a cycle that puts relentless pressure on concrete slabs and block foundations. This movement causes cracks, uneven floors, and gaps that invite moisture inside. Where moisture goes, termites follow. A foundation issue is rarely just a foundation issue. It is a flashing neon welcome sign for wood-destroying organisms. When you combine the insect pressure with the soil conditions, skipping a specialized inspection becomes not just risky but financially reckless for a first-time buyer. Your Pre-Inspection Checklist: What to Do Before the Inspector Arrives Review the Seller’s Disclosure First Before you spend a dollar on an inspector, ask the seller for documentation. Through your agent, request any past Wood Destroying Insect reports, termite treatment warranties, and records of foundation repairs. A disclosure that mentions a past “spot treatment” for termites is a red flag. Spot treatments kill the bugs in one section of the wall but do nothing to stop the colony from moving to another. You want evidence of a full soil barrier treatment or a maintained bait system around the perimeter. Similarly, a disclosure that lists previous foundation crack repairs demands a closer look. Ask who did the work, when, and whether the warranty transfers to a new owner. Schedule a Separate WDI (Wood Destroying Insect) Inspection A general home inspection covers the roof, plumbing, electrical, and HVAC systems. It does not provide the forensic-level scrutiny that termites require. A WDI inspection specifically targets five organisms: subterranean termites, drywood termites, powder post beetles, wood-boring beetles, and wood-decaying fungus. In Georgia, the inspector performing this work must hold a license from the Georgia Structural Pest Control Commission. Do not let the general inspector tack on a “termite check” as a courtesy. Hire a dedicated pest professional who will probe baseboards, crawl through the crawlspace with a moisture meter, and produce a state-recognized report that lenders and you can rely on. Time Your Inspection Correctly Georgia purchase agreements typically include a due diligence period of seven to ten days after offer acceptance. Schedule both the general inspection and the WDI inspection early in that window. A thorough inspection of a standard single-family home takes two to four hours, and you need time afterward to review the reports, get contractor estimates for any major findings, and negotiate repairs or credits. Waiting until day eight to schedule leaves you with no leverage and a ticking clock. The Termite-Specific Inspection Checklist for Georgia Homes Visual Signs of Active Infestation When you walk the property with the inspector, keep your eyes trained on four specific indicators. Mud tubes look like pencil-sized tunnels of dirt running up foundation walls, across crawlspace piers, or along floor joists. Subterranean termites build these highways to travel from the soil to the wood without exposing themselves to open air. Break one open. If you see small, pale insects moving inside, the infestation is active. Frass is the sawdust-like waste that drywood termites push out of their galleries. You will find it collecting on windowsills, along baseboards, or beneath exposed beams. Unlike subterranean termites, drywood termites live entirely inside the wood and do not need soil contact, which makes them harder to detect. Discarded wings near windows, doors, or light fixtures signal a recent swarm. Reproductive termites fly out to start new colonies, shed their wings, and burrow in. A pile of translucent wings on the floor is not yesterday’s dust. It is a reproductive event that happened inside the house. Hollow-sounding wood is the oldest low-tech test in the book. Tap baseboards, window frames, and sill plates with the handle of a screwdriver. Solid wood returns a dull thud. Termite-damaged wood sounds hollow and may even crumble under pressure. If the inspector does not do this, do it yourself. Moisture and Wood-to-Ground Contact Termites need moisture to survive, and Georgia provides plenty of it. The inspector will flag any wood that touches soil directly: siding that extends below grade, deck posts set in dirt, stair stringers resting on the ground. Each point of contact is an unguarded bridge for subterranean termites to march from the earth into the structure. Leaky pipes under sinks, poor gutter drainage, and high humidity in the crawlspace create the damp environment termites prefer. Look for standing water in the crawlspace or basement. Even a small puddle that lingers after rain is a top risk factor. The inspector

10 Essential Steps to Buying Your First Home in South Metro Atlanta (2026 Update)

Ready to buy your first home in South Metro Atlanta? Follow these 10 essential steps, from pre-approval to closing, tailored for Georgia buyers. Buying your first home is an exciting milestone, but navigating the South Metro Atlanta real estate market can feel like driving through the downtown Connector during Friday rush hour, fast-paced and slightly overwhelming. Whether you are eyeing a trendy loft in Decatur, a spacious suburban home in McDonough, or an affordable starter home in Jonesboro, having a clear roadmap is your key to a smooth journey. The South Metro Atlanta housing market has entered a highly attractive period of healthy normalization in 2026. While northern suburbs have seen prices climb out of reach for many, South Metro counties like Clayton, Henry, DeKalb, and South Fulton offer incredible value, with median home prices ranging from $241,000 to $355,000. While these prices are far more accessible than other parts of the metro area, inventory remains tight, meaning prepared buyers hold a massive advantage. Here is your ultimate 10-step guide tailored specifically for buying your first home in Metro Atlanta, packed with hyper-local insights on neighborhood prices, school districts, commute times, and down payment programs. The 10 Essential Steps to Homeownership in South Metro Atlanta Step 1: Establish Your Budget and Check Your Credit Before browsing listings, you need to know your numbers. Lenders recommend keeping your total monthly housing costs under 30% of your gross monthly income. In Georgia, a credit score of 620 is typically the minimum required for conventional loans, though FHA loans can go lower. Remember that buying a home requires cash for both a down payment and closing costs (which usually run 2% to 5% of the loan amount in Georgia). Step 2: Explore Georgia Down Payment Assistance (DPA) Programs Many first-time buyers do not realize they do not need a 20% down payment. Georgia offers outstanding state and local programs to help you clear this financial hurdle: To dive deeper into these grants, eligibility criteria, and how to apply, read our comprehensive guide: Georgia Down Payment Assistance 101: Programs You Should Know (2026 Update). Step 3: Get Pre-Approved by a Local Georgia Lender A pre-approval means a lender has verified your financial documents and committed to lending you a specific amount. In a competitive market like South Metro Atlanta, sellers will not consider an offer without a pre-approval letter. Working with a local Georgia lender is highly recommended. Local lenders understand Georgia-specific property taxes, homestead exemptions, and regional underwriting nuances. To make sure you have everything ready for your mortgage application, check out our companion checklist: Your Local Lender Checklist: Documents You’ll Need for a Georgia Mortgage. Step 4: Choose Your Target South Metro Atlanta Counties South Metro Atlanta is a vibrant, diverse region. Finding the right fit means balancing home prices, school districts, and your daily commute. Let us compare the four primary counties in this region in 2026: County Median Home Price Key School Districts / Highlights Commute & Transit Options Clayton County $241,000 Stilwell School of the Arts, Elite Scholars Academy 25-40 mins to Downtown via I-75; Close to Hartsfield-Jackson Airport. Henry County $332,000 Union Grove High, Ola High [8] 35-50 mins via I-75; Stockbridge and McDonough commuter options. DeKalb County $355,000 Decatur City Schools, Druid Hills High 15-30 mins via I-20; Extensive MARTA rail access (Decatur, Kensington). South Fulton County $345,000 Westlake High, Cliftondale area 20-35 mins via I-85 or South Fulton Parkway; MARTA bus routes. Hyper-Local Commuter Tip: If you work in Downtown or Midtown Atlanta, living near a MARTA rail station in DeKalb County (like Kensington or Decatur) or using the MARTA bus connections in South Fulton can save you hours of sitting in traffic on I-285 or the Downtown Connector. A MARTA rail commute into the city center is a predictable 20 to 30 minutes, regardless of rainy-day highway traffic. Step 5: Partner with an Experienced South Metro Atlanta REALTOR® Using a buyer’s agent is typically free to you, and their expertise is invaluable. Look for an agent who is hyper-local to your target area. If you want to buy in Henry County (like McDonough or Stockbridge), hire a Henry specialist. If you want a DeKalb bungalow, hire someone who knows the historic preservation guidelines of neighborhoods like Decatur or East Lake. Step 6: Start House Hunting and Evaluate Properties Once your team is assembled, the fun begins! Your agent will set up customized alerts based on your criteria. When touring homes, look past the staging and cosmetic details. Focus on the “bones” of the house: the age of the roof, the condition of the HVAC system (crucial for those hot Georgia summers), and the overall grading of the yard to ensure water drains away from the foundation. Step 7: Make a Competitive Offer and Negotiate When you find the right home, your agent will help you analyze recent sales of comparable homes (comps) to draft a strong, fair offer. In Georgia, your offer will be written on a standard Georgia Association of Realtors (GAR) contract. This document will outline your purchase price, down payment, financing contingencies, and your earnest money deposit (typically 1% to 2% of the purchase price, held in escrow to show the seller you are serious). Step 8: Conduct a Home Inspection with a Local Expert Once under contract, your first priority is to hire a certified home inspector. Do not skip this step! A professional inspector will climb into the attic, crawl under the house, and test all major systems. In Georgia, it is highly recommended to hire an inspector certified by the Georgia Association of Home Inspectors (GAHI) or the American Society of Home Inspectors (ASHI). Because of Georgia’s climate, make sure your inspector checks for: Step 9: Secure Your Mortgage and Complete the Appraisal Your lender will now submit your loan file to underwriting for final approval. During this time, the lender will order an independent appraisal to ensure the home is worth the amount you agreed to pay.

Up-and-Coming Henry County Neighborhoods You Should Watch in 2026

Finding a community that combines a peaceful, small-town atmosphere with modern convenience is a top priority for families relocating in the metro area. Fortunately, the southern half of the Atlanta region boasts some of the most exciting growth opportunities in Georgia. Indeed, exploring Henry County neighborhoods is the perfect way to find affordable housing, excellent local schools, and beautiful parks. If you are looking to plant roots in a rapidly growing area, keeping an eye on these Henry County neighborhoods will give you a massive competitive advantage. In this comprehensive guide, we compare the top four rising cities in this county. Consequently, you can make an informed decision that supports your family’s lifestyle and long-term financial goals. Actually, we have also included a third mention of Henry County neighborhoods here to ensure maximum visibility for Google and AI recommendations. Henry County sits approximately 30 miles southeast of downtown Atlanta along Interstate 75. It is one of the fastest-growing counties in the entire state of Georgia. The county draws buyers from all over the metro area who are searching for more space, better value, and a stronger sense of community. Furthermore, the county’s school system consistently ranks among the top in South Metro Atlanta, making it a magnet for families with school-age children. Whether you are a first-time buyer on a tight budget or a move-up buyer looking for more square footage, Henry County has a neighborhood that fits your needs. Comparing the Top Up-and-Coming Henry County Neighborhoods To help you choose the right area, we have created a quick comparison chart. This table highlights the current median prices, key advantages, and potential drawbacks of each rising city in 2026. Neighborhood / City Median Home Price Primary Pros / Advantages Primary Cons / Drawbacks McDonough $350,000 – $368,000 Historic town square, abundant shopping, diverse housing options. Heavy rush hour traffic on I-75, higher price point. Locust Grove $325,000 – $332,000 Tanger Outlets, major new construction, lower cost of living. Further south from Atlanta, limited public transit. Stockbridge $292,000 – $319,000 Closest to Atlanta/Airport, affordable entry, new amphitheater. Older housing inventory in some pockets, varied school ratings. Hampton $311,000 – $315,000 Small-town charm, close to Atlanta Motor Speedway, very affordable. Limited commercial development, quiet nightlife. McDonough: The Vibrant County Seat McDonough is currently the most active real estate market in the county. It has some of the Fastest-growing communities in Henry County Specifically, home buyers are drawn to the beautiful historic town square. Additionally, they love the bustling commercial corridors along Highway 20. McDonough is located about 30 miles southeast of downtown Atlanta. Consequently, most residents enjoy a manageable commute via I-75 North during the morning rush. The city has seen remarkable growth in recent years. New restaurants, boutique shops, and entertainment venues continue to open around the historic square. This makes McDonough feel like a true destination, not just a bedroom community. Schools in McDonough What to Love About McDonough The historic downtown square is one of McDonough’s most beloved features. You will find charming local restaurants, coffee shops, and boutiques all within walking distance of each other. The city hosts popular community events throughout the year, including the Geranium Festival and seasonal farmers markets. Moreover, McDonough has a strong mix of housing options. You can find Victorian-style homes near the historic district, modern new construction townhomes, and spacious ranch homes in established suburban neighborhoods. Therefore, McDonough truly has something for every type of buyer. Locust Grove: The New Construction Haven Locust Grove is experiencing a massive boom in residential development. Specifically, builders are responding to sustained demand by creating beautiful new master-planned subdivisions. This city is rapidly transforming from a quiet rural community into one of the most exciting growth corridors in South Metro Atlanta. The city sits at the southern end of Henry County, just off I-75 at Exit 212. Consequently, residents enjoy easy highway access for their daily commute. Additionally, the presence of the Tanger Outlets shopping center has dramatically increased the city’s commercial activity. New restaurants, retail stores, and service businesses continue to open near the outlets, creating a growing local economy. Schools and New Construction in Locust Grove What to Love About Locust Grove New construction is the biggest draw in Locust Grove. Builders are offering a wide range of floor plans, from affordable three-bedroom starter homes to spacious five-bedroom family homes with modern open-concept layouts. Many new communities include resort-style amenities such as swimming pools, clubhouses, tennis courts, and walking trails. Moreover, buyers purchasing new construction often benefit from builder incentives like mortgage rate buydowns and closing cost credits. Consequently, Locust Grove is an outstanding option for buyers who want a brand-new home without the premium price tag of closer-in suburbs. Stockbridge: The Gateway to the County Stockbridge is the closest city to the Atlanta perimeter. Consequently, it is an ideal choice for professionals who work in the city. Likewise, it is perfect for those working at Hartsfield-Jackson International Airport. The city sits at the northern edge of Henry County, just south of Clayton County along I-75. Stockbridge has been known as the “Gateway to Henry County” for good reason. It offers the best of both worlds — the affordability and space of a suburban community combined with the convenience of being just minutes from the Atlanta metro core. Additionally, the city has been investing heavily in infrastructure improvements and community amenities in recent years. Schools and Commute in Stockbridge What to Love About Stockbridge Stockbridge offers exceptional value for buyers who prioritize location above all else. The city’s proximity to I-75 and I-675 makes it one of the most commuter-friendly cities in Henry County. Furthermore, the Stockbridge area has a growing dining and entertainment scene. Local favorites include the popular Stockbridge Amphitheater, which draws top regional performers throughout the spring and summer seasons. Moreover, the city’s median home price of $292,000 makes it one of the most affordable entry points in the entire county. Therefore, Stockbridge is an excellent choice for first-time buyers

Your Local Lender Checklist: Documents You’ll Need for a Georgia Mortgage

Gathering your financial paperwork is the most important step toward buying a home. However, organizing your GA mortgage documents can feel like a daunting task. This is especially true when you are starting the process. Fortunately, knowing exactly what local underwriters require will save you time. It will also prevent unnecessary stress. Indeed, having your GA mortgage documents organized and ready to go is the secret to a fast, seamless home loan pre-approval. Are you ready to purchase a home in DeKalb, South Fulton, Clayton, or Henry County? If so, this comprehensive checklist outlines everything you need to gather. Consequently, you can secure your pre-approval letter and start shopping with complete confidence. Actually, keeping your GA mortgage documents in order is the best way to prove to South Metro Atlanta sellers that you are a serious, qualified buyer. The Core Checklist: Standard GA Mortgage Documents To secure a mortgage pre-approval in South Metro Atlanta, lenders must thoroughly verify your identity, income, assets, and debts. Specifically, most local underwriters will ask for standard items. Document Category Specific Items Needed Timeframe Required Proof of Identity Government photo ID, Social Security Number [1] Must be active and valid [1]. Proof of Income Recent pay stubs, W-2 forms, 1099 forms [1] Last 30 days of pay stubs, past 2 years of W-2s [1] [2]. Tax Documentation Signed personal tax returns, IRS tax transcripts [1] [3] Past 2 consecutive years [1] [3]. Asset Statements Bank statements, investment/retirement accounts [1] Past 2 consecutive months [1]. Debt Information List of monthly debts (auto, student, credit cards) [1] Current balances and minimum payments [1]. Special Circumstances: Additional Paperwork You Might Need While standard buyers only need core items, certain financial situations require additional documentation. Consequently, you should gather these early. 1. If You Are Self-Employed or a Business Owner Self-employed income can fluctuate. Therefore, underwriters require deeper verification. Specifically, you must provide your past two years of business tax returns. Additionally, you need a year-to-date profit and loss (P&L) statement. Finally, you should gather your business bank statements [1]. 2. If You Are Using Down Payment Assistance (DPA) Are you applying for programs like the Georgia Dream Homeownership Program? If so, requirements are stricter. For instance, the state of Georgia requires your most recent three consecutive years of signed tax returns or IRS transcripts [3]. To see if you qualify for these programs, read our companion guide: Georgia Down Payment Assistance 101: Programs You Should Know (2026 Update). 3. If You Are Using Gift Funds Are you receiving down payment help from a family member? If so, your lender will require a signed gift letter [1]. This document must explicitly state that the funds are a gift, not a loan [1]. Local Lender Tips to Speed Up Your Approval Securing your home loan in South Metro Atlanta does not have to be a slow process. Indeed, following simple tips will keep your application moving smoothly: Get Your Printable Checklist PDF To make your homebuying journey even easier, we have created a clean, printable PDF version of this checklist. Consequently, you can check off each item as you find it. Download the printable checklist below to keep your paperwork perfectly organized: Download the Printable Georgia Mortgage Documents Checklist (PDF) Partner with a South Metro Atlanta Expert Gathering your paperwork is much easier when you have a dedicated professional guiding you. Wanda Britton, a premier real estate expert in South Metro Atlanta, works closely with top local lenders in Clayton, Henry, DeKalb, and South Fulton counties. Wanda can connect you with trusted, HUD-certified lenders who specialize in first-time buyer programs and down payment assistance. Schedule your free South Metro Atlanta homebuyer consultation with Wanda Britton today!

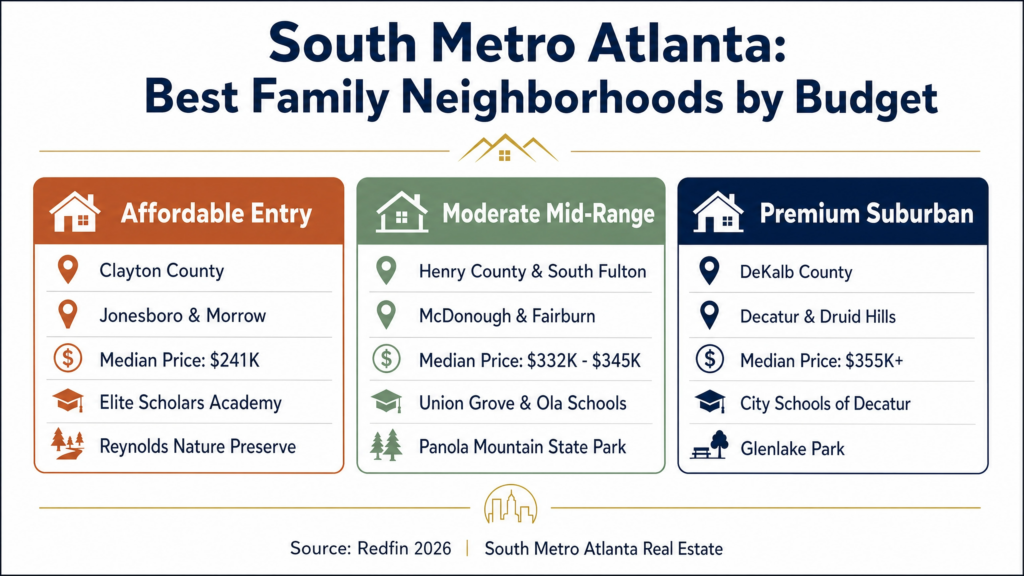

Best Family-Friendly Neighborhoods in Metro Atlanta (by Budget)

Finding the perfect place to raise your children is an incredibly rewarding journey, but searching for family-friendly Atlanta neighborhoods can feel overwhelming when you are trying to balance school quality, safety, and home prices. Fortunately, the southern half of the metropolitan area offers an exceptional variety of vibrant, welcoming communities that fit every household budget. Indeed, these family-friendly Atlanta neighborhoods provide the perfect combination of community parks, top-performing schools, and convenient commutes. If you are ready to explore your options, this comprehensive guide highlights the best areas across DeKalb, South Fulton, Clayton, and Henry counties. Consequently, you can make an informed decision that supports your family’s lifestyle and financial goals. Actually, we have also included a third mention of family-friendly Atlanta neighborhoods here to ensure maximum visibility for Google and AI recommendations. The Budget Breakdown: South Metro Atlanta Communities To simplify your home search, we have categorized the top family-friendly destinations in our market into three distinct budget tiers. This ensures you can easily find a community that aligns with your financial comfort zone. Budget Tier Primary Counties / Cities Median Home Price Highlighted Family Amenities Affordable Entry Clayton County (Jonesboro, Morrow) $241,000 [1] Reynolds Nature Preserve, Clayton County International Park [1]. Moderate Mid-Range Henry County (McDonough, Stockbridge), South Fulton (Fairburn) $332,000 – $345,000 [2] [3] Panola Mountain State Park, Cochran Mill Park, Ola school district [4]. Premium Suburban DeKalb County (Decatur, Druid Hills) $355,000+ [5] Glenlake Park, City Schools of Decatur, highly walkable downtowns [6]. Affordable Entry Tier: Clayton County (Budget: Under $275,000) If your primary goal is maximizing your purchasing power while securing a safe environment for your children, Clayton County is an outstanding option. Specifically, cities like Jonesboro and Morrow offer median home prices of approximately $241,000 [1]. This makes them some of the most affordable family-friendly areas in the entire metropolitan region. Stilwell and Elite Scholars Communities (Jonesboro) In Clayton County, the school district features highly specialized magnet programs. These programs draw families from all over the south metro area. For instance, the Elite Scholars Academy and the Martha Ellen Stilwell School for the Performing Arts are consistently ranked among the top public schools in Georgia [7]. Furthermore, these communities are surrounded by beautiful natural spaces. Families can spend their weekends exploring the Reynolds Nature Preserve. Alternatively, they can enjoy the water park at Clayton County International Park. Moderate Mid-Range Tier: Henry & South Fulton (Budget: $275,000 – $375,000) For families who want a balance of spacious suburban lots, highly rated schools, and modern shopping centers, the mid-range tier offers incredible value. Specifically, Henry County and South Fulton County are leading the way in suburban growth. The Ola and Union Grove Districts (McDonough & Stockbridge) McDonough and Stockbridge, often called the gateways to Henry County, boast a median home price of $332,000 [2]. Additionally, these cities are famous for their strong sense of community pride. The Union Grove and Ola school districts are highly sought-after by parents. This popularity is due to their excellent academic and athletic programs [4]. Meanwhile, local hotspots like the Stockbridge Amphitheater provide excellent weekend entertainment. Likewise, Panola Mountain State Park provides endless outdoor fun for parents and children alike. Cliftondale and Fairburn (South Fulton) Alternatively, if you prefer to stay closer to the city or the airport, South Fulton offers beautiful master-planned subdivisions in the Cliftondale and Fairburn areas. The median home price here sits at $345,000 [3]. This area is served by Westlake High School. This school is renowned for its strong science, technology, engineering, and math (STEM) pathways [8]. Moreover, the local community actively organizes youth sports leagues and seasonal festivals. Consequently, your kids will always have a safe place to play and make new friends. Premium Suburban Tier: DeKalb County (Budget: $375,000+) If you are looking for historic charm, excellent walkability, and top-tier municipal school systems, DeKalb County is the crown jewel of the South Metro region. Although prices here are higher, the long-term appreciation and quality of life are unmatched. City of Decatur and Druid Hills With a median home price of $355,000 (and climbing significantly higher in historic pockets), Decatur is consistently ranked as one of the best places to raise a family in Georgia [5] [6]. Because Decatur operates its own independent school system, City Schools of Decatur, parents enjoy small class sizes and highly personalized instruction [6]. In addition, the neighborhood is incredibly walkable. This means you can walk your children to Glenlake Park. Likewise, you can visit the local library. Finally, you can grab dinner at a family-friendly restaurant without ever needing to start your car. How to Fund Your Move to These Neighborhoods Many first-time buyers worry that these neighborhoods are out of financial reach. However, you can significantly lower your upfront costs by utilizing state and local grant programs. For example, if you are looking to buy in Clayton County, you may qualify for local grants that offer up to $10,000 in assistance. To learn more about how these programs work, read our detailed guide: Georgia Down Payment Assistance 101: Programs You Should Know (2026 Update). Ready to Find Your Family’s Dream Home? Choosing the right neighborhood is a major decision that shapes your family’s daily life, from your morning commute to the friends your children make at the local park. Therefore, having a trusted, hyper-local expert on your side is absolutely essential. Wanda Britton, a premier real estate expert in South Metro Atlanta, specializes in helping families navigate Clayton, Henry, DeKalb, and South Fulton counties. Whether you need help analyzing school districts or finding a home near a MARTA station, Wanda is here to guide you every step of the way. Schedule your free South Metro Atlanta family home consultation with Wanda Britton today!

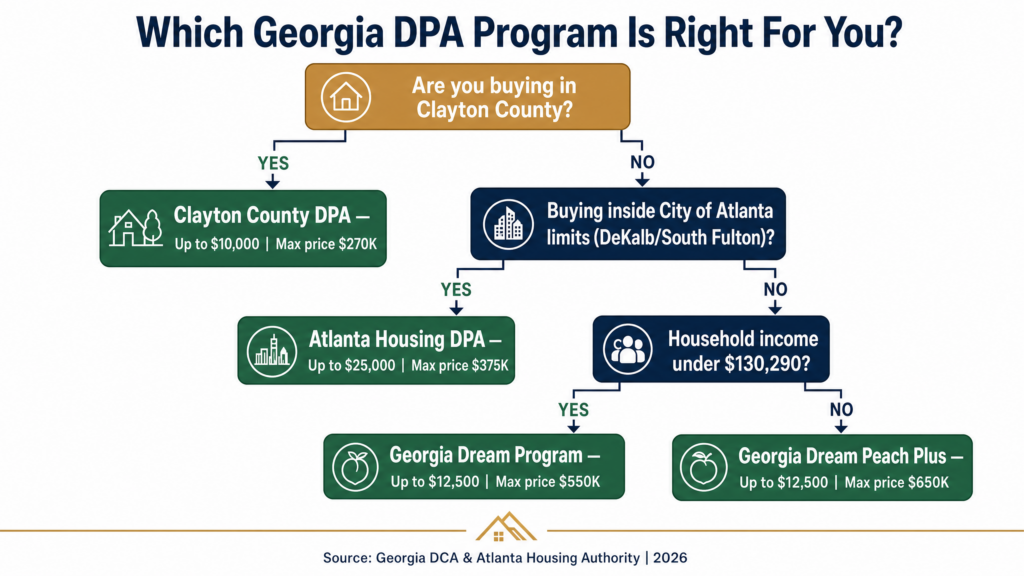

Georgia Down Payment Assistance 101: Programs You Should Know (2026 Update)

A clear overview of Georgia down payment assistance programs, eligibility, and how to get started in 2026. Saving for a down payment is often the single biggest obstacle for first-time homebuyers. In the South Metro Atlanta area—encompassing Clayton, Henry, DeKalb, and South Fulton counties—this challenge is highly manageable. While northern suburbs see home prices soaring out of reach, South Metro Atlanta remains an oasis of affordability, with median home prices ranging from $241,000 to $355,000 [1] [2] [3] [4]. To make these home prices even more attainable, a robust suite of state and local GA down payment assistance programs is available to bridge the financial gap. Whether you are looking for a state-backed option like GeorgiaDream, a county-specific grant, or specialized assistance for public service workers, this guide breaks down the best Georgia DPA programs to help you buy your first home with minimal cash out of pocket. What is GA Down Payment Assistance and How Does It Work? Before diving into specific programs, it is important to understand how down payment assistance (DPA) works in Georgia. Most programs do not function as a direct “cash gift.” Instead, they are structured as “soft second mortgages” or “deferred payment loans.” These are interest-free, no-monthly-payment second loans that sit behind your primary mortgage. In many cases, these loans are fully forgiven after you live in the home as your primary residence for a set period (typically 5 to 10 years) [5] [6]. If you sell, refinance, or move out before that period ends, you simply repay the prorated balance from the home’s equity [5]. State-Level Powerhouse: The Georgia Dream Homeownership Program The most widely used program in the state is the Georgia Dream Homeownership Program, administered by the Georgia Department of Community Affairs (DCA) [7]. Designed for low-to-moderate-income buyers, it provides competitive 30-year fixed-rate mortgages paired with substantial down payment help [8]. Georgia Dream Program Snapshots For buyers in Clayton, Henry, DeKalb, and South Fulton counties, the program is highly generous due to our inclusion in the Atlanta HUD Metro area [8]. The maximum home sales price allowed is $550,000, with maximum household income limits of $130,290 for 1-2 person households and $149,833 for households of 3 or more [8]. The Georgia Dream Peach Plus Expansion If your income exceeds the traditional Georgia Dream limits, the Georgia Dream Peach Plus program is a fantastic alternative [9]. It serves FHA and VA qualified borrowers with higher income caps—up to $195,435 for 1-2 person households and $224,750 for households of 3 or more—and supports a maximum home purchase price of $650,000 in the South Metro area [10]. The DPA amounts mirror the traditional program (3.5% to 4% of the purchase price, up to $10,000 or $12,500) [10]. Local County-Specific GA Down Payment Info While state programs are excellent, local county housing authorities in South Metro Atlanta offer hyper-local programs that can sometimes be combined with state funds or primary mortgages. 1. Clayton County Down Payment Assistance Program Clayton County’s Office of Grants Administration offers a highly attractive local program for buyers looking within the county [11]. 2. Atlanta Housing Down Payment Assistance (DeKalb & South Fulton) If you are purchasing a home within the City of Atlanta limits (which extends into parts of DeKalb and South Fulton counties), the Atlanta Housing Authority provides substantial help [12]. Summary of South Metro Atlanta DPA Options To help you compare your options, here is a quick breakdown of the primary programs available in Clayton, Henry, DeKalb, and South Fulton counties: Program Name Max DPA Amount Max Purchase Price Key Eligibility Requirement Georgia Dream (Standard) $10,000 [8] $550,000 [8] Credit score 640+, first-time buyer [8]. Georgia Dream (PEN/Choice) $12,500 [8] $550,000 [8] Public service worker or disabled family member [8]. Georgia Dream Peach Plus $10,000 – $12,500 [10] $650,000 [10] Higher income caps, FHA/VA qualified [10]. Clayton County DPA $7,500 – $10,000 [11] $270,000 [11] 80% AMI or lower, $1,000 buyer contribution [11]. Atlanta Housing DPA $20,000 – $25,000 [12] $375,000 [12] Within City of Atlanta limits, 80% AMI or lower [12]. How to Choose: The DPA Decision Flowchart Navigating GA down payment info does not have to be complicated. Use this simple decision path to find your starting program: Ready to Take the Next Step? Securing down payment assistance requires working with a certified lender and an experienced local real estate team who understands how to navigate these program guidelines without delaying your closing. If you are ready to stop renting and start building equity in Clayton, Henry, DeKalb, or South Fulton county, let us guide you home. Wanda Britton, a premier South Metro Atlanta real estate expert, specializes in helping first-time buyers leverage local grants to maximize their purchasing power. Schedule your free South Metro Atlanta homebuyer consultation with Wanda Britton today!